Long before this summer when health plan cancellation notices began arriving in plan member mailboxes, health insurers were creating alternative plan options for their consumers. The Patient Protection and Affordable Care Act (ACA), signed into law March 25, 2010 and upheld by the Supreme Court in 2012, was a guarantee that health plans for millions of Americans would become obsolete by January 1, 2014. The lack of media and industry attention regarding health plan design requirements and repeated political commitments stating consumers could keep existing health plans have resulted in confusion and frustration. Individuals and small businesses impacted by the health insurance plan cancellations are scrambling to understand coverage options.

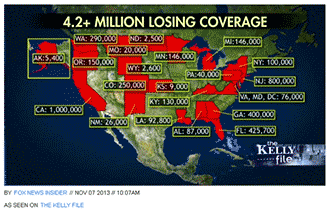

According to White House spokesman Jay Carney pointing to a June 2010 edition of the Federal Register, 5% of the population – or somewhere between 12-15 million people who had individual or small group health insurance policies – will be required to change health plans to be compliant with ACA.

Health plan design changes

The ACA outlines ten essential health benefits which health plans much include as of January 1, 2014.

- Ambulatory patient services (outpatient care you get without being admitted to a hospital)

- Emergency services

- Hospitalization (such as surgery)

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services

Source: Healthcare.gov

Regardless of personal need or applicability or gender, all health plans are required to include the ten essential health benefits. Health plans are no longer allowed to charge a higher premium for females, as all plans are required to have maternity care coverage. Plans are no longer allowed to deny coverage due to pre-existing medical conditions. And health plans must also allow dependent children to remain on the plan until the age of 26.

If a policy lacks the ten essential health benefits and was issued before the new law was passed by Congress in 2010, it may be grandfathered in and avoid cancellation. Policies obtained after the law was passed are subject to cancellation and the holder of the policy must obtain a new health plan which meets the minimum standards.

Alternative health plan options

ACA required insurers to provide 90-day notice to policyholders receiving health plan cancellations. Consumers receiving cancellations are provided alternative health plan options from their insurance carrier with the cancellation notice. Higher-rate policy options may be presented and are often the result of the richer benefits in the new plan as compared to the cancelled health plan. Lower fees are common for consumers with pre-existing medical conditions who were previously paying a higher premium to gain access to a health insurance plan.

Savvy consumers will not accept the alternative health plan from their current insurer without comparing plans available locally and on the state and federal exchanges. Considerations for a new plan may include assessing and comparing plan options, including:

- Healthcare providers and health system inclusion in the plan

- In-network and out-of-network provisions

- Health premium, co-payment requirements and plan deductible payments

What’s next?

As has been widely reported, the federal marketplace’s HealthCare.gov has been plagued with technical problems and the federal government says it hopes to have HealthCare.gov working smoothly for most users by the end of the November, though it’s not clear that target will be met. And even though fewer than 10% of Americans will gain access to health plans through the federal marketplace, the insureds receiving cancellations are within the pool of citizens to benefit from the plans and potential subsidies.

The obvious solution to increase enrollment and help cancelled members shop for new healthcare coverage is for the federal government to fix the HealthCare.gov exchange website. But if the exchange is not fixed by the end of the month, there are alternative solutions:

- Use of alternative government sign-ups through mail and telephonic enrollment

- Direct sign-up with marketplace approved insurance companies

- Extend enrollment window or delay individual mandate

- Preserve non-grandfathered plans

The White House promises it is planning additional solutions. Aside from having the site fixed by the end of the month, options presented thus far are complex and bring with them several potential problems.

Recently, the White House provided an administrative fix to resolve the cancellation of healthcare coverage for more than 12-15 million insureds. The federal administration will allow insurers to extend healthcare coverage until 2014 to those policyholders originally slated for cancellation. In short, policyholders who were receiving healthcare coverage that do not meet the ACA standards will be grandfathered in for an additional year. The White House encourages those who get cancellation letters to look for coverage in the federal exchange and potentially find better options, including government subsidy.

As we continue to address healthcare reform in future blog posts, I invite you to join the discussion. Join my LinkedIn group – Transforming Healthcare for Tomorrow – and share your thoughts.

Kimberly George, SVP, Senior Healthcare Advisor

Sources:

- https://www.healthcare.gov/what-does-marketplace-health-insurance-cover/

- http://www.forbes.com/sites/theapothecary/2013/10/31/obama-officials-in-2010-93-million-americans-will-be-unable-to-keep-their-health-plans-under-obamacare/

- http://www.npr.org/blogs/itsallpolitics/2013/11/14/245092637/6-ideas-being-floated-to-fix-obamacare-sign-up-woes