As drones gain in popularity, there are a number of ideas and opportunities for them to add value to the insurance industry. They can prove valuable in disaster response efforts, underwriting surveys, claims investigations and in situations where aerial photography is needed. As interest in drones grows throughout the country, there are several challenges for businesses to address. To benefit from this advanced technology, companies will need to define their operational processes, services and usage, while complying with the Federal Aviation Administration (FAA).

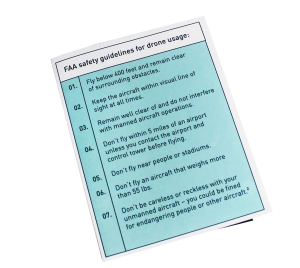

FUN FOR HOBBYISTS, VALUABLE FOR BUSINESSES With the expanded use of drones on the horizon, the FAA has been updating the rules for flying them. Beginning December 21, 2015, individuals who fly small unmanned aircraft for recreational use will be required to register them with the FAA. Existing owners will have to register by February 19, 2016 and new buyers will have to register before their first flight.1 In addition, the FAA strongly encourages drone operators to follow the safety guidelines below:

1. Fly below 400 feet and remain clear of surrounding obstacles.

2. Keep the aircraft within visual line of sight at all times.

3. Remain well clear of and do not interfere with manned aircraft operations.

4. Don't fly within 5 miles of an airport unless you contact the airport control tower before flying.

5. Don't fly near people or stadiums.

6. Don't fly an aircraft that weighs more than 55 lbs.

7. Don't be careless or reckless with your unmanned aircraft - you could be fined for endangering people or other aircraft.2

Flying an unmanned aerial vehicle for any non-hobby or non-recreational purpose requires FAA authorization. For example, using a drone to take aerial photos of your backyard for personal use is recreational, but using it to take photographs to sell is non-recreational. In addition to obtaining approval to fly a drone for commercial use, the operator must have a minimum of a sport pilot certification as well as a spotter who must be able to keep the drone in their line of sight.3

As state legislatures evaluate how the technology should be regulated, the benefits of their use, the economic impact and privacy concerns are among the key areas being considered.4

In the underwriting and claims investigation arenas, drones provide several key advantages. They can be used in pre-loss valuations to gather images of mechanical/industrial equipment on top of large commercial structures or difficult to navigate places, or to survey crops and land for agricultural exposures. After an event such as a hail storm or hurricane, drones can be used to assess the scope and extent of damage to real property and provide a clearer depiction of the magnitude of the loss. They can take in more information and gather it quicker than adjusters can through the standard process; not just for a single loss location, but also when handling multiple loss locations or large property exposures. For example, if an insurance carrier has a client with losses in areas that were subjected to either wind or flooding due to a hurricane, a drone can be utilized to inspect all of the locations that match specific GPS coordinates and gather images for data collection. This data can then be reviewed, processed and analyzed in conjunction with meteorological data. The technology and capabilities of the drone would increase efficiency and decrease cycle time, leading to quicker payments for policyholders.

Sedgwick was recently approved to use drones and our next steps will include defining the service offering and the operational process. If the FAA continues to require commercial users to have a pilot’s certification or be on private, approved property, it will restrict the application for drone usage in our industry. We will continue developing services that will be integrated with our property liability solutions while monitoring the evolving FAA requirements.

Scott Richardson

SVP, National Property Manager, Vericlaim, a Sedgwick company

Additional Resources

This content was originally published in the edge edition 003. To read more articles like this click here http://edge.sedgwick.com/issue...